Caps and Closures Market - Industry Analysis, Market Size, Share, Trends, Application Analysis, Growth And Forecast 2022 - 2027

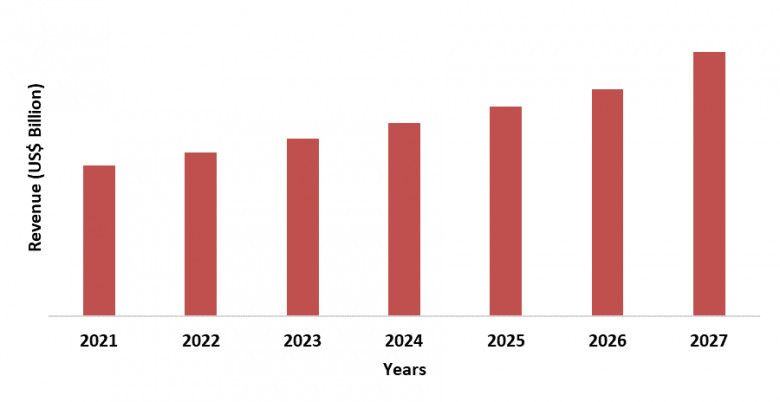

Caps and Closures Market size is forecast to reach US$85.3 billion by 2027, after growing at a CAGR of 5.3% during 2022-2027. Caps and closures are plastic packaging on top of bottles, jars, tubes, cans, and so on. Caps and closures are of different types such as screw top, corks, metal crowns, Snap-On, friction fit, tamper-evident, and dispersing. Caps and closures find a broad range of applications in numerous industries such as beverages, cosmetics, and pharmaceuticals. The increasing bottled water and the packaging from the pharmaceutical industry are mainly driving the market growth during the forecast period.

The material used to manufacture caps and closures must possess an excellent balance of stiffness and toughness along with good chemical resistance. Factors such as stringent regulations in the caps and closures industry with regards to the use of plastic caps and closures as well as growing demand for the substitute packaging options, such as blister packaging options are factors that are expected to affect the growth of the global caps and closures market. The widely used material for manufacturing caps and closures are polyethylene terephthalate (PET), polypropylene (PP), High-Density Polyethylene (HDPE), and others. The growing consumers’ demand for convenience products is one of the major factors driving the market growth during the forecast period.

Inquiry Before Buying - https://www.industryarc.com/reports/request-quote?id=19083

Covid-19 Impact

The outburst of the covid-19 has specified several extraordinary challenges to all manufacturers and production companies. The caps and closures industries also confronted a lot of difficulties in assembling plastic and receiving the workforce as the whole world was under quarantine. The gathering of the raw material and the delivery of the end product all was at stake during the lockdown. However, after a while, the market was back to normal when certain rules were changed. With the change where everyone around the world has to turned into extra aware of environmental safety. As the lifestyles have transformed people are choosing to be healthier and more sustainable after the pandemic.

Report Coverage

The Report : “Caps and Closures Market – Forecast (2022-2027)”, by IndustryARC, covers an in-depth analysis of the following segments of the Caps and Closures Industry.

By Material Type : Plastic (Polyethylene Terephthalate (PET), Polypropylene (PP), High-Density Polyethylene (HDPE), Low-density polyethylene (LDPE), and Others), Metal (Steel, Aluminum, and Others), and Others

By Product Type : Easy-open Can Ends, Metal Lug Closures, Peel-off Foils, Plastic Screw Closures, Metal Crowns, Metal Screw Closures, Corks, Plastic Screw Closures, and Others

By Type : Continuous Thread Closures, Dispensing Closures, Tamper-Evident Closures, Bar-Top Closures, Child-Resistant Closures, and Snap-On Closures

By Application : Beer, Wine, Bottled Water, Carbonated Soft Drinks, and Others

By End-use Industry : Packaging, Food Packaging, Beverages Packaging, Personal care, and Cosmetics Packaging, Pharmaceutical packaging, Toiletries Packaging, and Others

By Geography : North America (USA, Canada and Mexico), Europe (UK, France, Germany, Italy, Spain, Russia, Netherlands, Belgium, and Rest of Europe), APAC (China, Japan, India, South Korea, Australia and New Zealand, Indonesia, Taiwan, Malaysia and Rest of APAC), South America (Brazil, Argentina, Colombia, Chile, Rest of South America), and Rest of the world (Middle East and Africa)

Key Takeaways

- Asia Pacific dominates the caps and closures market owing to a rapid increase in the packaging sector.

- Rising demand for bottled water is expected to drive the demand for caps and closures over the forecast period.

- The growing demand for pharmaceutical packaging is driving the market for caps and closures during the forecast period.

- Stringent government regulation on banning polymer products is hampering the market growth.

Caps and Closures Market Segment Analysis - By Material Type

The plastic segment holds the largest share in the caps and closures market in 2021 and is forecast to grow at 5.6% CAGR during 2022-2027. Caps and closures are made using several types of rugged polymers, including polyethylene terephthalate (PET), Polypropylene (PP), High-Density Polyethylene (HDPE), Low-density polyethylene (LDPE), and others. Caps and closures provide a safe, secure way to ship medicines and small consumer items, offering additional protection when goods are transported inside custom cardboard boxes. Owing to its advantages like cost-effectiveness, Food and Drug Administration (FDA) approved the plastics make it the most preferable material in the caps and closures manufacturing and certainly escalate the growth of the market.

Caps and Closures Market Segment Analysis - By End-Use Industry

The food packaging segment holds the largest share in the caps and closures market in 2021 and is forecast to grow at 4.5% CAGR during 2022-2027. Owing to the rapid industrialization and urbanization, there is an unprecedented endorsement for packaged food across the world especially in developing countries such as India and China. The growing demand for bottled drinks is made mostly by PET, due to their versatility in shape and size. It is entirely recyclable and also the highest recycled plastic worldwide.

It is recycled by carefully washing and re-melting it, or by chemically breaking it down to its component materials to make new PET polymer. For instance, the Canada PET recycling rate was 27.9% in 2019. The rising demand for polyethylene terephthalate in food and beverages packaging such as carbonated soft drinks packaging contributed to the growth of the caps and closures market. The growing significance of packaging in the food industry is eventually propelling the growth of the plastic caps and closure market since the caps and closure are prominent parts of the packaging and play vital role in preserving the quality of the food packed.

Caps and Closures Market Segment Analysis - By Geography

Increase demand for Bottled Water

The Demand from Pharmaceutical Packaging Sector is Driving the Market

Packaging of healthcare products reduces the possibility of product contamination and protects healthcare products from moisture, gas, light and temperature. This is driving the demand for caps and closures in the pharmaceutical end-use sector. After the pandemic, the demand for healthcare facilities, medicine related products are in high demand and eventually growing daily. For instance, in 2020 Mondi, UK based packaging company has recently developed packaging for QIAGEN's SARS-CoV-2 coronavirus test kit consisting of a polyester, aluminum, polyethylene packaging, and caps construction to provide the necessary protection from light and moisture so that the test kits are not compromised before they are used.

The development in the healthcare sector is driving the caps and closures market rapidly for like, the French fund Lauxera Capital Partners, which was launched in 2020 in Paris and San Francisco, announced a US$121 million fund to support European healthcare startups. Whereas, in India, the government invested US$8.80 billion outlay for the healthcare sector over six years in the Union Budget 2021-22 to strengthen the existing National Health Mission by developing capacities of primary, secondary, and tertiary care, healthcare systems, and institutions for detection and cure of new & emerging diseases. With the rapid growth rate in the healthcare sector, the demand for caps and closures will parallelly increase and certainly have a positive impact on the caps and closures market.

Stringent Government Regulations and Banning of Polymer Products Impede Market Growth

The FDA has pressurized manufacturers to submit data regarding the long-term health impact of inorganic substances in Plastics particularly hormonal effects and contributors to anti-biotic resistant bacteria, to ascertain the safety of medical use Plastics products like gloves. The most common plastic in use to produce containers and caps and closures of packed drinking water is polyethylene terephthalate (PET), which takes 400 years to naturally decompose in nature.

While these plastics are highly recyclable, less than half the bottles sold are collected for recycling and just 7% of them are being recycled. Due to its low cost, easy transportation, low weight, and high resistance as well as lack of taste and aesthetic problems, PET is widely used for packaging a wide variety of edible products including water. As plastic bottles are not readily biodegradable, the main challenge is their durability in the environment. The discarded PET bottles have a high potential to be an environmental catastrophe, especially in economically developing countries if not recycled sufficiently. Thus, hampering the market growth of caps and closures in the forecast period.

Caps and Closures Industry Outlook

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the market. Caps and Closures top 10 companies include:

- RPC Group Plc (UK)

- Reynolds Group Holdings Limited (New Zealand)

- Crown Holdings Inc. (U.S.)

- Amcor Limited (Australia)

- Rexam PLC (UK)

- Berry Plastics Corporation (U.S.)

- Silgan Holdings Inc. (U.S.)

- AptarGroup Inc. (U.S.)

- Guala Closures Group (Italy)

- BERICAP GmbH Co. & KG (Germany).

Recent Developments

- In 2020, Borealis and MENSHEN combined launched a technology that unites the Borealis recycling and compounding expertise with its own. These packaging solutions are predominantly made for use in laundry and home care and include also 2K closures.

Related Reports:

Cosmetic Packaging Market - Forecast(2022 - 2027)

Report Code: CPR 0108

Aerosol Caps Market - Forecast(2022 - 2027)

Report Code: CMR 55780